The Long Tail of CRM: Why 20+ CRMs Still Thrive Beyond Salesforce & HubSpot (2026)

Salesforce and HubSpot own under half the CRM market. Here's why the long tail of 20+ best-of-breed and vertical CRMs keeps winning in 2026.

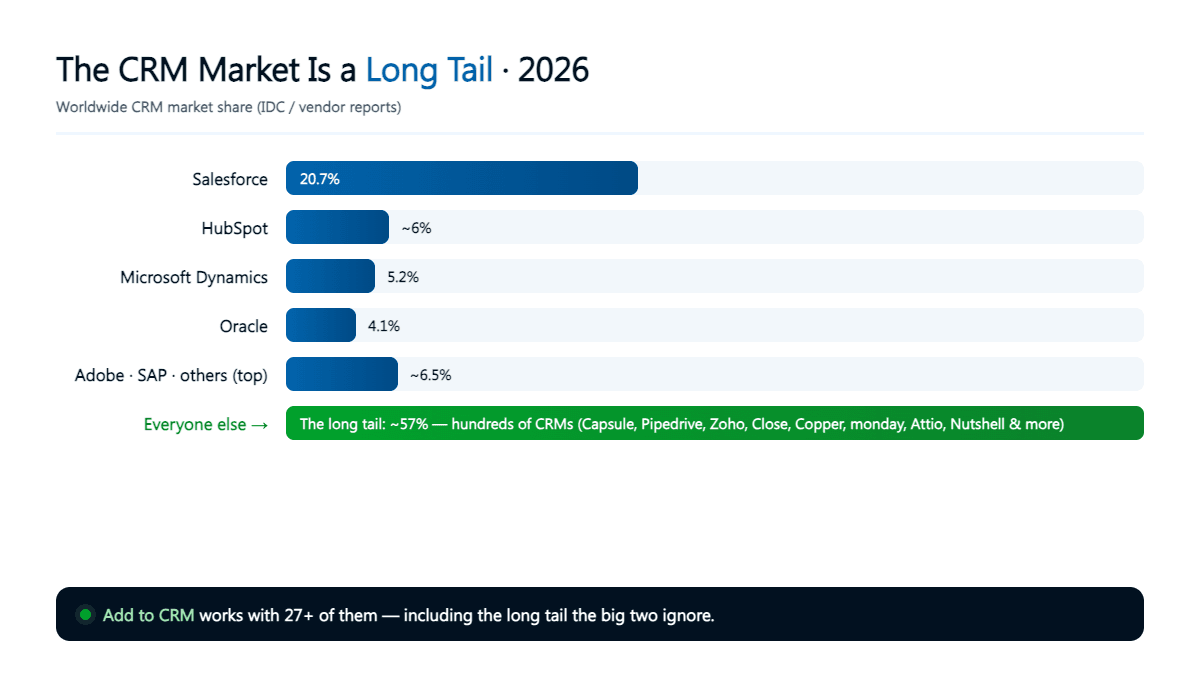

Because the CRM market only looks like a two-horse race. As of mid-2026 Salesforce holds about 20.7% of the worldwide market and HubSpot 5–6%; even with Microsoft, Oracle, Adobe and SAP added in, the named leaders reach barely 40%. The other 55–60% is a "long tail" of hundreds of CRMs that keep winning on fit, price and simplicity.

TL;DR: The two most famous CRMs own less than half of their own market. The rest is a fragmented long tail of best-of-breed and vertical tools — Capsule, Pipedrive, Zoho, Close, Copper, monday, Attio, Nutshell, Salesflare, Less Annoying CRM and more — that keep winning because fit, price and simplicity beat brand recognition. If your CRM isn't Salesforce or HubSpot, you're in the majority.

For a decade, choosing a CRM has felt binary: Salesforce or HubSpot. But the two most talked-about CRMs don't dominate their market — they lead a field so fragmented that "everyone else" outweighs every household name combined. Here's why that long tail exists, why it keeps winning, and what it means for buyers and the tools that serve them.

The CRM market isn't a two-horse race — here's the data

According to IDC's worldwide CRM market tracker — the figures most widely cited across analyst and vendor reports — Salesforce is the clear leader as of mid-2026 at roughly 20.7% of worldwide CRM revenue, reportedly larger than its next several rivals combined. HubSpot is the fastest-growing of the majors at around 5–6%: its own investor figures put it near 299,000 customers, about $3.45B in annual recurring revenue, growing roughly 28% year over year. After that, shares drop off quickly.

| Vendor | Approx. worldwide CRM market share (mid-2026) | Notable context |

|---|---|---|

| Salesforce | ~20.7% | Market leader, by a wide margin |

| HubSpot | ~5–6% | Fastest-growing major vendor (~28% YoY); ~299,000 customers; ~$3.45B ARR |

| Microsoft Dynamics 365 | ~5.2% | Bundled into the wider Microsoft ecosystem |

| Oracle | ~4.1% | Enterprise suites and customer-experience clouds |

| Adobe | ~3.4% | Experience Cloud, marketing-led |

| SAP | ~3.1% | Enterprise CX tied to ERP |

| Everyone else — the long tail | ~55–60% | Hundreds of CRMs: Zoho, Pipedrive, Capsule, Close, Copper, monday, Attio, Nutshell, Salesflare, Less Annoying CRM, and many more |

Add the six most prominent vendors together and you reach barely 40% of the market. The remaining 55–60% — well over half — belongs to no single name. It's split across hundreds of CRMs, from challengers like Zoho and Pipedrive down to industry-specific systems most people outside a given vertical have never heard of.

And this isn't a small or shrinking pie. Industry analysts value the global CRM software market at more than $80 billion in 2026, rising to around $130 billion by 2030. A majority share of a market that size is an enormous amount of software that is neither Salesforce nor HubSpot.

A note on sources: market-share percentages are based on IDC's worldwide CRM tracker as summarised across analyst and vendor reports; HubSpot's customer, revenue and growth figures come from its own investor disclosures; market-size estimates are from independent analysts. Figures are approximate and current as of mid-2026 — vendor share moves every reporting period, so treat them as a snapshot, not a scoreboard.

What "the long tail" actually means

The phrase comes from Chris Anderson's 2004 observation that when distribution and choice become cheap, demand stops concentrating in a few hits and spreads across a huge number of niches. Plot a market as a curve and you get a few tall bars on the left — the hits — and a long, low tail stretching to the right that, added up, outweighs the head.

CRM fits the pattern almost perfectly. There is no single "right" way to manage customer relationships, because a solo consultant, a 12-person agency and a 5,000-seat software company are not doing the same job. Each niche has enough specific needs — and enough willingness to pay for a tool that fits — to sustain its own CRM. The result: a head of two or three giants and a tail of dozens of viable, profitable, genuinely well-loved products.

Why the long tail of CRM persists

If the big platforms had simply won, the tail would be shrinking. It isn't — and the reasons are structural, not sentimental.

Fit beats feature count. Most teams use a small fraction of an enterprise CRM's capabilities, yet still pay for and navigate all of it. A tool built around one clear job — Pipedrive's visual deal pipeline, Copper's Google Workspace record-keeping, Salesflare's automatic inbox logging — often gets used, where a general-purpose giant gets abandoned. In CRM, adoption is the whole game: a system nobody updates is worse than a spreadsheet.

Price and total cost of ownership. Enterprise CRMs get expensive quickly once you add seats, editions, add-on clouds and the implementation partner to wire it all together. Long-tail CRMs frequently cost a fraction of that with no consultant required. Less Annoying CRM has built an entire identity on flat, transparent, low pricing — evidence that "cheap and simple" is a durable position, not a temporary one. (Prices change; check the vendor's site for current numbers.)

Simplicity and time-to-value. An SMB doesn't have a full-time Salesforce administrator. It has a founder who wants leads in the system by Friday. Tools you can set up in an afternoon win that buyer decisively — and the switching-cost moat that protects incumbents barely applies when onboarding takes a day.

Industry specificity. Horizontal giants treat vertical workflows as configuration problems; vertical CRMs treat them as the product. Agencies gravitate to Copper, services businesses to Capsule, high-velocity inside-sales teams to Close (with calling and SMS built in). When your CRM already speaks your industry's language, you don't have to bend it into shape first.

The SMB majority. The overwhelming majority of businesses on earth are small. They vastly outnumber enterprises, don't buy like enterprises, and together represent a colossal amount of CRM demand. The long tail isn't a rounding error — it's where the numerical majority of businesses live.

New entrants keep arriving. The tail also regenerates. Attio's data-model-native design, monday's work-OS foundation and folk's lightweight approach are all recent answers to "the incumbents don't work the way we do." Every time the category's defaults ossify, someone ships a fresh take — and finds an audience.

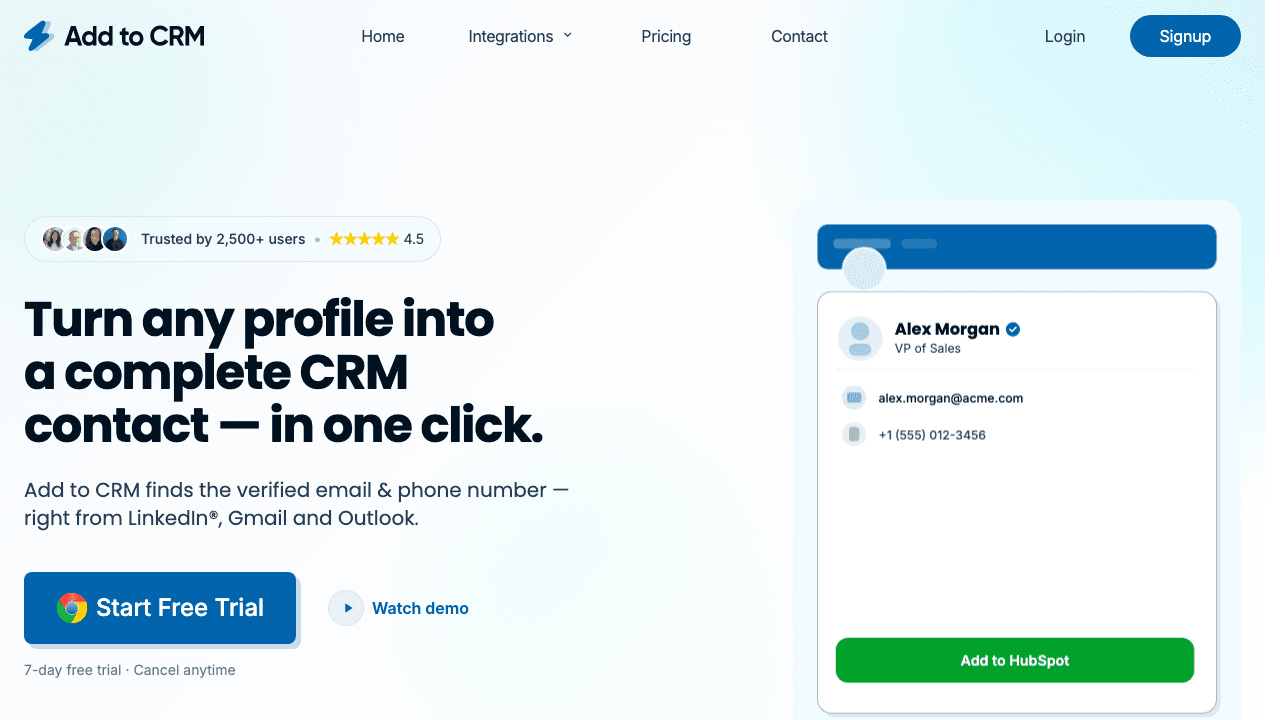

Turn LinkedIn® profiles into CRM contacts

Add to CRM finds verified emails, phone numbers, and job titles on LinkedIn® — then adds them to your CRM in one click.

Start Free TrialMeet the long tail: the CRMs most teams actually run

"The long tail" sounds abstract until you name it. These are real, widely used CRMs that sit outside the big two — each strong at a specific job:

| CRM | Best known for | Typical user |

|---|---|---|

| Zoho CRM | Broad features and value inside a full business suite | Cost-conscious teams wanting an all-in-one |

| Pipedrive | Visual, deal-first sales pipeline | Sales-led SMBs |

| Capsule | Simple, relationship-focused record-keeping | Small teams and consultancies |

| Close | Built-in calling and SMS for high-velocity sales | Inside-sales and SDR teams |

| Copper | Deep Google Workspace integration | Agencies and Google-native teams |

| monday CRM | Flexible work-OS foundation | Cross-functional teams |

| Attio | Data-model-native, highly customisable | Modern startups and ops-led teams |

| Nutshell | Straightforward pipeline plus email marketing | SMB sales teams |

| Salesflare | Inbox-native, automatic activity logging | Solo founders and small B2B teams |

| Less Annoying CRM | Flat pricing and radical simplicity | Solopreneurs and very small businesses |

None of these is a fringe product — several have hundreds of thousands of users. What they share is a refusal to be all things to all people, and that focus is why their customers choose them over a bigger, broader alternative.

But isn't the CRM market consolidating?

It's a fair challenge, worth taking seriously. Some analysts argue the market is consolidating: buyers are tired of stitching together a dozen tools, and platform vendors are bundling CRM with marketing, service, data and now AI into a single "customer platform." At the enterprise end, that pressure is real — big companies genuinely are rationalising their stacks.

But there's a difference between a company consolidating its own tools and the vendor market consolidating onto a few winners. The first is happening; the second largely isn't. The SMB majority optimises for fit and simplicity, not suite breadth — a bundled everything-platform is exactly what those buyers don't want. "Consolidation" at the top often just means a giant acquiring a niche player and running it as a separate product — which doesn't reduce the number of distinct CRMs in the wild. And every consolidation wave triggers an unbundling wave: today's long-tail tools were often yesterday's answer to bloated suites. The head may get taller; the tail isn't disappearing.

What the long tail means if you're choosing a CRM

The practical takeaway is liberating: you don't have to default to the famous option. A few principles:

- Choose for fit and adoption, not brand recognition. The best CRM is the one your team will actually keep up to date. If a simpler, cheaper, better-fitting tool wins on that, it wins.

- Right-size, don't over-buy. Paying enterprise prices for capabilities you'll never switch on is a common, expensive mistake. Match the tool to the job you have now.

- Weigh total cost, not sticker price. Implementation, admin time and add-ons often dwarf the per-seat line; long-tail CRMs frequently win on the full bill.

- Protect your data portability. Make sure you can get your contacts in and out cleanly — which is where the tooling around your CRM matters as much as the CRM itself.

27 CRMs supported. Try free for 7 days

Add to CRM finds verified emails, phone numbers, and job titles on LinkedIn® — then adds them to your CRM in one click.

Start Free TrialWhat the long tail means for the tools that serve you

Here's the twist most buyers discover only after they've chosen. The moment your CRM isn't Salesforce or HubSpot, much of the surrounding software ecosystem quietly stops working for you. Plenty of enrichment and sales tools integrate with only a handful of the biggest CRMs — often just the two at the head of the curve, plus maybe Pipedrive. Pick Capsule, Close, Nutshell or Attio and you're frequently told to export a CSV and import it by hand.

That's the real cost of the tooling world ignoring the long tail: the majority of the market gets second-class support. It's exactly the gap Add to CRM was built to close.

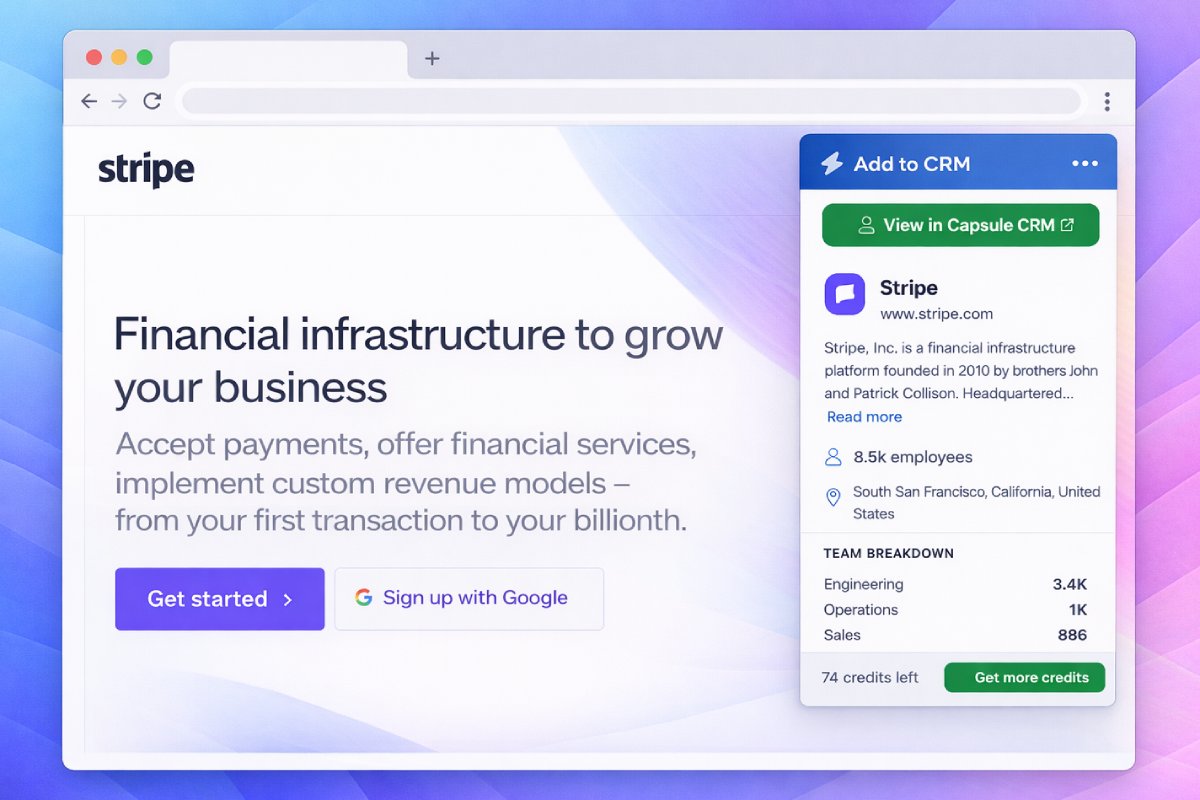

Add to CRM is a Chrome extension that enriches a contact from a business network, Gmail, Outlook or a company website — returning a verified email, phone number and 20+ data points — and adds the complete record to your CRM in one click. Crucially, it works with 27+ CRMs, not just the two at the top: Capsule, Pipedrive, Zoho, Close, Copper, monday, Attio, Nutshell, Salesflare, Less Annoying CRM and many more (the full list is on the integrations page). Connect your CRM once, and every field maps to the right place automatically — no CSV round-trip.

That breadth is a deliberate bet on the shape of the market: if the long tail is where most businesses run their sales, the tooling around the CRM should meet them there — not force them onto a giant to get decent support.

Frequently asked questions

What percentage of the CRM market do Salesforce and HubSpot control? As of mid-2026, Salesforce holds roughly 20.7% of the worldwide CRM market and HubSpot about 5–6%, per IDC-based figures. Even adding Microsoft, Oracle, Adobe and SAP, the named leaders together reach only around 40% — leaving 55–60% to the long tail of everyone else.

What is the "long tail" of CRM? It's the large collection of smaller and more specialised CRMs that, added together, hold the majority of the market. No single one is huge, but collectively they outweigh the household names — because different businesses have genuinely different needs.

Is the CRM market consolidating? At the stack level, yes — many companies are reducing tool sprawl, and platform vendors are bundling aggressively. But the vendor market stays fragmented, because the SMB majority keeps choosing best-fit tools and new entrants keep appearing. Consolidating a buyer's stack isn't the same as consolidating the market.

What are the best CRMs that aren't Salesforce or HubSpot? Widely used options include Zoho, Pipedrive, Capsule, Close, Copper, monday, Attio, Nutshell, Salesflare and Less Annoying CRM. "Best" depends entirely on your workflow, budget and industry — which is the whole point of the long tail.

Why would a business pick a smaller CRM over Salesforce? Usually fit, price and simplicity. Smaller CRMs are faster to set up, cheaper to run, and often shaped around a specific way of selling — which drives the adoption that makes any CRM worthwhile.

Can I use enrichment and prospecting tools with a long-tail CRM? Sometimes — but many tools only integrate with the biggest one or two CRMs. Add to CRM supports 27+, so you can enrich and add contacts to Capsule, Close, Nutshell, Attio and dozens more without exporting a CSV.

One click, any CRM. The long tail is where most teams actually work — so your tooling should too. Add to CRM enriches contacts with verified emails, phone numbers and 20+ data points and adds them to any of 27+ CRMs in one click. Start a 7-day free trial and add your first contact in under two minutes.

Start saving time and closing more deals.

Find contact info for your prospects on the #1 business social network and add them to your CRM with 1-click.

Trusted by 1000s of founders, SDRs & more